Breaking SR&ED News: The CRA Unveils New T661 Form

Reference Article (>5 Years Old)Please note that the information herein may be outdated, links could be inactive, and policies discussed may have evolved. For the most current data, consult our latest publications. If you would like us to refresh this article as it is of interest to you, please contact us. |

After months of speculation, the Canada Revenue Agency (CRA) has finally revealed the new T661 form, which is used to apply for the Scientific Research & Experimental Development (SR&ED) tax credit. Claimants may submit the current form until the end of the year, but as of January 1, 2014 all submissions will be required to use the new version.

What are the changes to the T661 form?

Here are the adjustments that were made to the T661 form as listed on the CRA website:

- We have removed lines 223 to 229 in Part 2.

- We have removed lines 230 and 232 in Part 2. The relevant information from these lines is now requested on lines 620 and 622 in Part 7.

- We have removed lines 235 to 238 in Part 2.

- We have consolidated former Sections B and C in Part 2 so that all claimants answer the same three questions in Section B. We have also changed the order of the questions in Section B.

- We have introduced notes in Parts 3 and 4 to advise that expenditures for capital property or the right to use capital property can no longer be claimed after December 31, 2013.

- We have changed the descriptions for lines 350, 355, 390, and 504 to reflect that expenditures for capital property or the right to use capital property can no longer be claimed after December 31, 2013.

- We have changed the description for line 820 to accommodate the 10% reduction in the prescribed proxy amount (PPA) for the number of days after December 31, 2013, in the tax year.

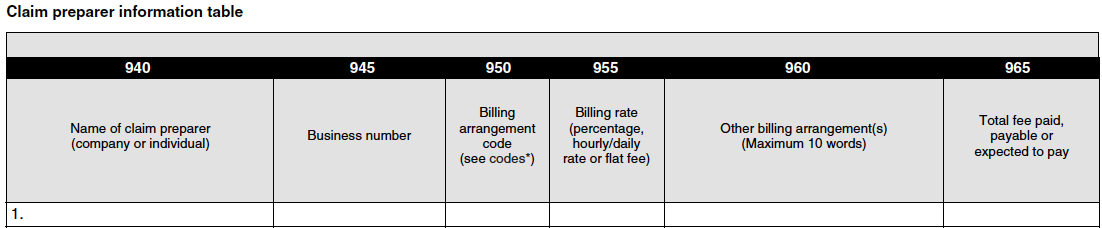

- We have introduced new Part 9 to capture SR&ED claim preparer information.

- Part 10 is formerly Part 9–Certification.

The most notable change to the T661 form is that claimants must now reveal previously private details about their SR&ED consultants; firms who help companies apply for SR&ED must now disclose sensitive information, such as billing arrangements and rates.