Maximum SR&ED refund: Federal level

We are often asked by our clients if there is a maximum Scientific Research and Experimental Development (SR&ED) refund that can be claimed. This is a great question and like most topics related to SR&ED, the answer is not straightforward. This article will explain the “maximum federal SR&ED refund” and how it may affect the investment tax credits (ITCs) your organization receives.

Federal Refund Rates for SR&ED

The federal refund rate available to SR&ED claimants depends on what type of corporation the claimant corporation is as well as the amount of eligible expenditures they are claiming for the tax year:

“Canadian-controlled private corporations: Generally, a Canadian-controlled private corporation (CCPC) can earn a refundable ITC at the enhanced rate of 35% on qualified SR&ED expenditures of $3 million. You can also earn a non-refundable ITC at the basic rate of 15% on an amount over $3 million. However, if you are a CCPC that also meets the definition of a qualifying corporation, you also earn a refundable ITC at the basic rate of 15% on an amount over $3 million, and 40% of the ITC can be refunded.” 1

If the $3M expenditure limit is exceeded only qualifying CCPCs are eligible to earn refundable ITCs over that limit. Other corporations may only earn non-refundable ITCs over the $3M expenditure limit. The term refundable refers to the credit that is reimbursed directly to the claimant, whereas non-refundable credit is applied to the taxpayers’ Part I tax, or carried back to a previous year and applied to the Part I tax in the previous year. Non-refundable tax credits are used only to reduce the amount of tax the claimant owes and are not returned in any monetary form to the claimant2. To learn how refundable and non-refundable ITC may be utilized at the end of the tax year see The Canada Revenue Agency’s SR&ED Investment Tax Credit Policy.

Maximum Federal SR&ED Refund: Running the Numbers

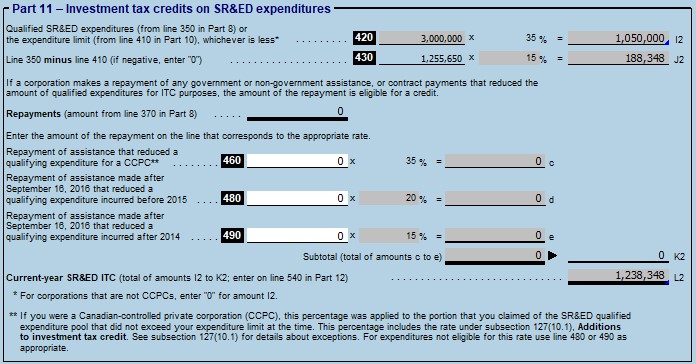

To see these calculations in practice we have included examples below. If the company is a CCPC using the Proxy method and has $3M of eligible expenditures for the tax year, then they will receive the enhanced rate (35%) on the initial $3M and the basic rate (15%) on the remaining amount of eligible expenditures, which includes the Prescribed Proxy Amount (PPA):

- In the example above line 420 includes the full $3M of expenditures made through the year (This also happens to be the expenditure limit for the enhanced ITC rate).

- 35% of $3M = $1,050,000

- Any expenditures over the $3M are placed in line 430.

- In this example, the expenditures over the $3M limit is $1,255,650 (In this example the overage consists entirely of the PPA that has been calculated) and only 15% of this amount is eligible as an ITC.

- 15% of $1,255,650 = $188,348

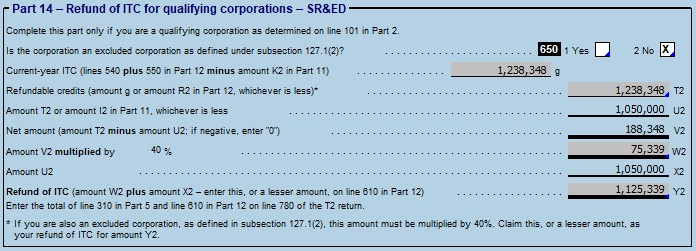

The $1,050,000 and $188,348 are combined and the full amount ($1,238,348) is transferred to Part 14 – Refund of ITC for qualifying corporations – SR&ED.

As mentioned, only 40% of the eligible “overage”(15%) is refundable. This means, in the example posed, the claimant would receive $75,339 back at the end of the year, while the remaining eligible ‘overage’ amount would be considered non-refundable and may be applied in a few ways as laid out in the SR&ED Investment Tax Credit Policy:

The claimant may apply in the current year, carry back, or carry forward their ITC to reduce their Part I tax otherwise payable according to the rules in sections 2.3.1 to 2.3.3. For certain entities, their ITC at the end of the tax year may be refunded (see section 4.0). 3

The calculations above detail how the refundable ITC is calculated:

- 40% of the eligible “overage”(15% of $1,255,650 = $188,348) is refundable.

- 40% of $188,348 = $75,339

- The ITCs earned on the $3M at the 35% enhanced rate, is added to the 40% of $188,348. The sum of these two amounts is the total ITCs to be refunded.

- $1,050,000 + $75,339= $1,125,339

Maximum Provincial Amounts

In this article, we only addressed the federal amounts. We would encourage you to look at the maximum amounts at the provincial level as well. For details of provincial R&D tax credit rates across Canada please visit our Provincial R&D Tax Credits – Interactive Map page. We have also summarized all the provincial R&D tax credit programs side-by-side for our readers in our article Provincial Tax Credits – Making the Most of SR&ED.

Conclusion

In conclusion, while the rate of return on refundable expenditures drops dramatically when over $3M, there are still available credits for those with expenditures that exceed $3M. For more information on rates for earning an SR&ED investment tax credit and how the expenditure limits are determined and allocated for Canadian corporations please review the SR&ED Investment Tax Credit Policy.