Non-arm’s length vs Arm’s length Contract Expenditures in SR&ED

*** This information is presented for educational purposes only and does not constitute legal advice. You should retain legal counsel if you require legal advice regarding your individual tax situation. ***

It is common for SR&ED projects to involve work contracted to professionals but, claiming contract expenditures for Scientific Research and Experimental Development (SR&ED) can be confusing. In this article, we will examine the difference between Non-arm’s length (NAL) vs Arm’s length contracts, how their respective expenditures will impact your SR&ED return, and how to complete the related SR&ED tax claim forms to increase your final SR&ED refund.

Before we delve into the minutiae of contract types, it is important to understand what exactly a contract for SR&ED is. The Contract Expenditures for SR&ED Performed on Behalf of a Claimant Policy describes a contract for SR&ED as:

An SR&ED contract is for the performance of basic research, applied research, experimental development, or support work, done on behalf of (see section 3.0) a claimant. For more information on what is SR&ED, refer to the Guidelines on the Eligibility of Work for SR&ED Tax Incentives.1

See our article Assistance and Contract Payments for SR&ED: Key Differences to understand the difference between contracts and financial assistance as these payments need to be claimed differently on the SR&ED forms.

Contract Expenditures for SR&ED

Contract expenditures may be claimed as an SR&ED expenditure and used to increase a claimant’s total SR&ED refund. This is stated in the CRA’s Assistance and Contract Payments Policy:

Where a Canadian claimant contracts to have SR&ED carried out on its behalf by another party, the amount payable under the contract may be a qualified SR&ED expenditure for investment tax credit (ITC) purposes.2

Up to 80% of an arms-length contract payment may be claimed as a qualified SR&ED expenditure:

Only 80% of the expenditure related to SR&ED contracts is allowable as a qualified SR&ED expenditure for the purpose of calculating the investment tax credit (ITC).3

The SR&ED tax forms will automatically remove 20% from contract expenditures, so be sure to enter the full value of the eligible SR&ED-related contract expenditures on your SR&ED tax forms.

Arm’s Length Contracts

‘Arm’s length’ refers to a situation where two parties that deal with each other are not related to each other and no control exists between them.4 With regards to SR&ED, the full amount of the SR&ED expenditures for an Arm’s length contracts are listed on the SR&ED forms, and 80% of these SR&ED contract expenditures are considered eligible:

Only 80% of the expenditure related to SR&ED contracts is allowable as a qualified SR&ED expenditure for the purpose of calculating the investment tax credit (ITC) to the extent that the SR&ED is performed in Canada in the tax year by a taxable supplier and is related to a business of the claimant.5

If the entirety of the SR&ED contract relates to the SR&ED work being completed on the claimant’s behalf then the entire amount paid for that contract should be listed on the SR&ED forms, however, if a portion of the expenditures were not related to SR&ED or if the expenses were incurred outside of Canada then “The portion of the contract amount that relates to non-SR&ED work is not allowed as an SR&ED expenditure and does not earn any ITCs.”6 The contract must be split between SR&ED and non-SR&ED work using a rational SR&ED allocation method. The contract performer (payee) is required to inform the claimant (payer) of what costs are non-SR&ED. This is referred to as the ‘look-through’ rule:

When a claimant is required to reduce an expenditure because of the look-through rule, the performer is required to inform the claimant in writing of the amount of the reduction. This information is to be provided without delay if requested by the claimant and in any other case no later than 90 days after the end of the calendar year in which the expenditure was made.7

We have detailed the look-through rule in our article SR&ED Contract Expenditures Outside of Canada.

Non-arm’s Length Contract

‘Non-arm’s length’ (NAL) refers to a situation where two parties that deal with each other are related and/or one party exerts control over the other. In other words, the parties are not dealing at arm’s length.8 Special rules apply to NAL contract expenditures:

… the claimant’s expenditures for the SR&ED contract are allowable SR&ED expenditures but are not qualified SR&ED expenditures for the purpose of calculating the investment tax credit (ITC).

The NAL performer can claim its SR&ED expenditures and qualified expenditures relating to the SR&ED work performed on behalf of (see section 3.0) the payer. Also, the amount received or receivable is not considered to be a contract payment and it will not reduce the NAL’s performer’s qualified expenditure for ITC purposes.9

The claimant may not claim SR&ED contract expenditures from a NAL contract, however, the performer of the contract may choose to either claim the expenditures themselves or to transfer all or a portion of the qualified SR&ED expenditures to the claimant:

Special rules may apply to allow the NAL performer to transfer all or a portion of its qualified SR&ED expenditures in the year to the payer up to a maximum of the contract amount. Use prescribed Form T1146, Agreement to transfer qualified expenditures incurred in respect of SR&ED contracts between persons not dealing at arm’s length, to make the transfer.10

The transfer of expenditures may only occur when the contract payments are “greater than the total qualified SR&ED expenditures that the recipient and the NAL party incurred in the year for the SR&ED.”11

It is important to note that a claimant cannot circumvent the NAL rules by including an arm’s length party between a payer and a NAL performer. To attempt to do so would be considered fraud.

SR&ED Tax Form Examples

In an effort to clarify how to claim your contract expenditures depending on whether they are arm’s length or NAL contract expenditures, we have detailed an example of each. For the sake of simplicity, both examples involve an Ontario-based CCPC which incurred $100,000 in SR&ED-related contract expenditures. No other expenditures have been listed in these examples.

Arm’s Length Example

The following example involves an Ontario-based CCPC which paid an Arm’s Length Contractor $100,000 to perform SR&ED on their behalf. In this example we have not listed any other costs, this means that while the claim utilizes the Proxy amount, no PPA is impacting the claim as the PPA is calculated by using a percentage of the salary base12.

The contractor costs must be manually entered in two places of the SR&ED claims. The first is on Line 340 of Schedule 32 – T661 – Claim for SR&ED, and the second is Line 756 of Schedule 60 – T661 Part 2 – Project information:

As “only 80% of the expenditure related to SR&ED contracts is allowable as a qualified SR&ED expenditure for the purpose of calculating the investment tax credit (ITC)”13 only $80,000 is used to calculate the final SR&ED ITCs. The provincial ITCs are deducted from the final total qualified SR&ED expenditures. In this example the total qualified SR&ED expenditures are calculated as below:

- Total expenditures = $100,000

- %80 of the contract expenditures = $80,000

- $80,000 – $8,976 (Provincial ITCs) = $71,024

The final Federal SR&ED ITCs available to the claimant in this example is 35% of those total qualified SR&ED expenditures, making the total $24,858:

Arm’s Length contract expenditures are fairly straightforward as none of the companies involved are directly related to each other. Non-arm’s Length dealing can be more confusing to claimants.

Non-arm’s Length Example

The following example involves an Ontario-based CCPC which paid a NAL Contractor $100,000 to perform SR&ED on their behalf. The NAL contractor costs must be manually entered in two places of the SR&ED claims. The first is on Line 345 of Schedule 32 – T661 – Claim for SR&ED, and the second is Line 756 of Schedule 60 – T661 Part 2 – Project information:

As NAL contract expenditures are “not qualified for the purpose of calculating the SR&ED ITCs“14, if the corporation claims their contractor expenditures in the same manner as an arm’s length contract expenditure they would have no total qualified SR&ED expenditures for ITC purposes and therefore, no available SR&ED ITCs for the tax year:

The Transfer of Qualified SR&ED Expenditures between NAL Corporations Using Form T1146

If the NAL performer chooses to do so they may transfer all or a portion of their qualified SR&ED expenditures in the year to the payer up to a maximum of the contract amount. In this case, prescribed Form T1146, Agreement to transfer qualified expenditures incurred in respect of SR&ED contracts between persons not dealing at arm’s length must be completed to make the transfer. To transfer SR&ED expenditures between non-arm’s length parties both must be performing and claiming SR&ED for the tax year and both must complete the T1146 form15. The T1146 is a short form but can be slightly confusing to understand and fill in correctly.

In this example the claimant is designated as the ‘transferee’, the entity that is receiving the qualified SR&ED expenditures:

The corporation’s details will prepopulate into the correct lines on this form. Tranferor details go in Lines 40-65, and the Transferee details go in Lines 70-95:

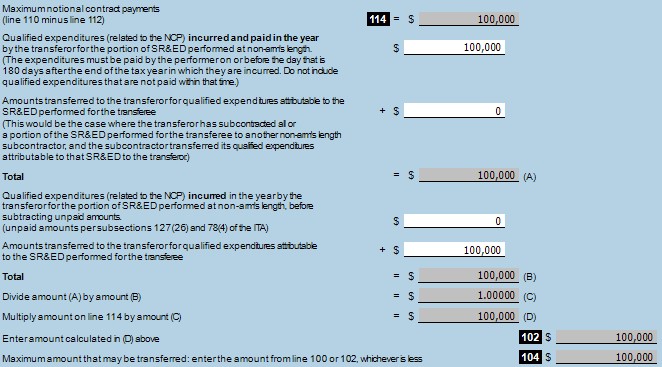

Next, the Transferor’s (the NAL subcontractor) SR&ED qualified expenditure pool before transferring money to the transferee is entered in Line 100:

In Line 110 the total contract amount agreed to be paid (Notional Contract Payment(NCP)) to the NAL subcontractor is entered. Keep in mind a transfer of expenditures is allowed “up to a maximum of the contract amount”16:

If any of the NCP is not paid within 180 days of the end of the FY, then the amount outstanding is entered into Line 112. This amount will reduce the total expenditures allowed to be transferred between corporations. In this example, the claimant paid the NAL performer the full contract payment of $100,000 within the tax year.

In the line directly under Line 114, the claimant must enter the total amount of the NCP that they did pay to the NAL performer within the allowed time frame. This amount also needs to be entered into the line above amount (B). These numbers are used to calculate the maximum amount that may be transferred. In this example, the NAL contractor was paid $100,000, all of which was attributable to the SR&ED performed on the payers’ (transferee’s) behalf. This mean they may choose to transfer the entire $100,000 of qualified expenditures back to the payer (transferee):

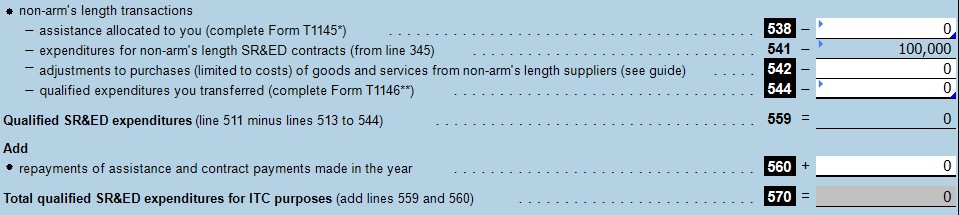

The claimant enters the amount of qualified expenditures being transferred to them on Line 106 which will then prepopulate into Line 508 of Form T661 – Claim for SR&ED:

- Line 492 is $100,000. This includes the NAL contract expenditure claimed in Line 345.

- Line 508 is the expenditures transferred to the claimant from the NAL corporation.

- Line 511 shows the contract expenditures plus the expenditures received for the tax year resulting in a total of $200,000 in expenditures being claimed.

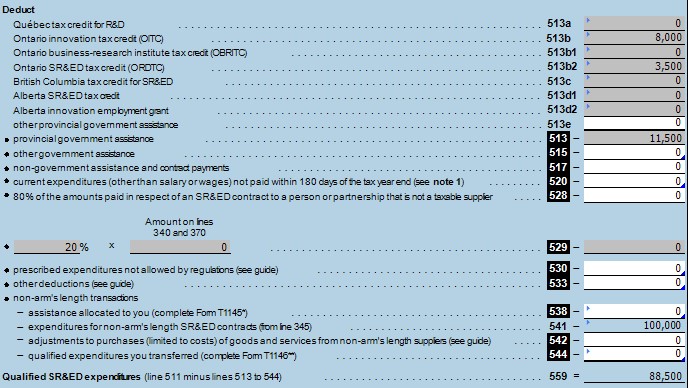

In Part 4 of Form T661, the provincial ITCs, totalling $11,500, and any NAL contract expenditures are subtracted as they do not count toward the total qualified SR&ED expenditures:

- $200,000 – $11,500 – $100,000 = $88,500

- The final Federal SR&ED ITCs available to the claimant in this example is 35% of those total qualified SR&ED expenditures, making the total $30,975:

Conclusion

It is quite common for SR&ED claimants to contract outside professionals/experts to assist in their SR&ED work, however, it is important to educate yourself on the difference between Non-arm’s length (NAL) vs Arm’s length contracts as each will uniquely impact your SR&ED return. If an arm’s length contract for SR&ED is entered into then the resulting contract expenditures may be claimed on your SR&ED tax forms. Arm’s length contract expenditures are fairly simple as 80% of those expenditures will count toward your total qualifying SR&ED expenditures for the purpose of calculating your final SR&ED ITCs. Non-arm’s length contracts often cause confusion because while these expenditures must be claimed on the T661 – Claim for SR&ED, the expenditures do not count towards the company’s total qualified SR&ED expenditures for the purpose of calculating their SR&ED ITCs. If the contracted NAL party is also claiming SR&ED for the tax year, they may agree to transfer some or all of their qualified SR&ED expenditures over to the NAL company which initially contracted them. Both companies must complete and file with their SR&ED forms their copy of Form T1146, Agreement to transfer qualified expenditures incurred in respect of SR&ED contracts between persons not dealing at arm’s length. As illustrated in our example, the transfer of qualified SR&ED expenditures can be useful in increasing the SR&ED ITCs receivable. There are many factors which will affect the decision to complete a transfer of expenditures. For example, if one corporation is a CCPC and the other is not, they may choose to transfer the contract expenditures to the CCPC entity in order to receive the enhanced 35% SR&ED refund rate. Be sure to weigh your options and ensure that you do not end up losing money. As always, we recommend you track all SR&ED-related expenditures as your SR&ED project progresses, this contemporaneous documentation will prevent any confusion when it is time to prepare your SR&ED tax forms and will help you if your claim is pulled for an audit.