SR&ED Form Comparison: The T661(12) vs. the New T661(13)

Reference Article (>5 Years Old)Please note that the information herein may be outdated, links could be inactive, and policies discussed may have evolved. For the most current data, consult our latest publications. If you would like us to refresh this article as it is of interest to you, please contact us. |

vs. the New T661(13)")

The Canada Revenue Agency (CRA) recently released the T661(13), the newest edition of the form used to apply for the Scientific Research & Experimental Development (SR&ED) tax credit. But how does the updated version compare to its predecessor, the T661(12)? We studied both versions and contrasted them for you below so you don’t miss any of the important changes.

For this article, we will be examining two aspects of the new forms. First, we’ll compare part 2 of the T661—also known as the technical narrative—to discover if there are any major changes. Second, we’ll look at the updated T4088—the document which provides detailed instruction on filling out the T661—to see if there has been any major upheavals within the guidelines.

Comparing Part 2 of the SR&ED Forms: T661s

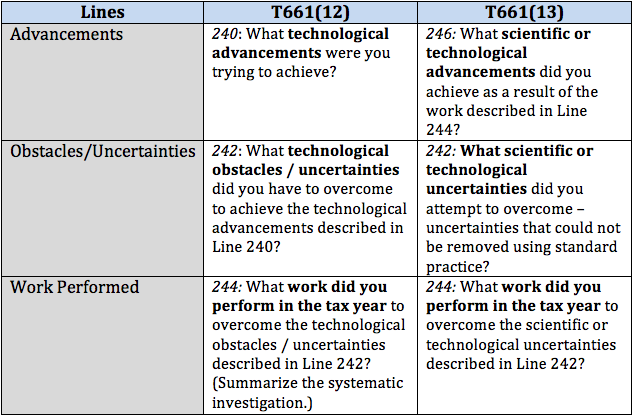

The wording within part 2 of the new T661 didn’t receive a big overhaul—though there are a couple interesting updates, which we’ll get to. The big change is that the lines have been reordered.

In summary, the technological advancements sections has been shuffled from its previous position (Line 240) to a new slot (Line 246) after the obstacles/uncertainties and work performed. Rather than beginning the technical narrative by outlining the technological advancements sought, claimants are now required to end the write-up by describing the advancements and how they specifically related to the work performed laid out in line 244.

The wording in part 2 hasn’t changed appreciably, though it’s interesting to note that Line 242 now clearly states that obstacles/uncertainties must “not be removed using standard practice.” This is a keystone of SR&ED, so the emphasis here is important.

Comparing the SR&ED SR&ED Forms: T4088s

The T4088 is a key SR&ED document that’s meant to give a clear explanation of how to fill out each section of the T661. Perhaps the biggest change is that the revised T4088 no longer lists its expectations in point form, making it much harder to pick out key information. For a program that requires extreme clarity, this is an unfortunate modification.

Below, we’ll do a side-by-side comparison to examine if there has been any important updates in wording when discussing the advancements, obstacles/uncertainties, and work performed.

Advancements

![T661(12) [Left], T661(13) [Right]](http://www.sreducation.ca/wp-content/uploads/2013/11/Screen-shot-2013-11-22-at-1.40.48-PM.png)

Previously, claimants used this space to set the stage for what was to come in the narrative; now, by focusing on the advancements specifically as they relate to the work performed, this section acts as a conclusion and final pitch as to why what was described in Line 244 was SR&ED work.

Obstacles/Uncertainties

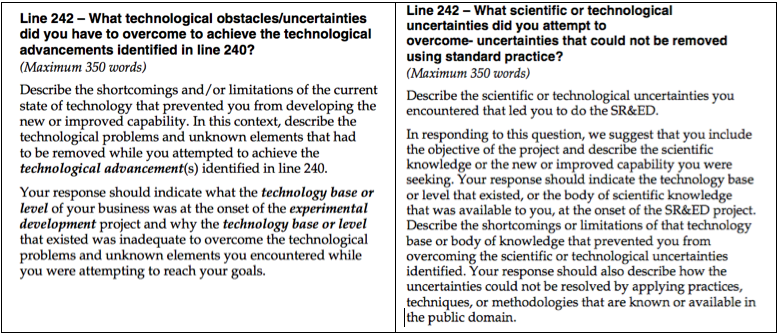

The changes to the instructions for Line 242 are subtle but meaningful. Firstly, as the opening section of the technical narrative, the T4088 states that this is now where the technological objectives should be stated. As this remains the area where the technology base has to be established, the CRA appears to be emphasizing that the technology base, technological objectives, and technological uncertainties are inextricably linked.

You will also note that the updated Line 242 instructions abandon the term “obstacle” altogether and choose to solely employ “uncertainty.” This is because “uncertainty” as a term has now been solidified in the Income Tax Act (ITA) through landmark court cases such as Northwest Hydraulic Consultants Ltd. v. The Queen (1998) and, more recently, Jentel Manufacturing Ltd. v. The Queen. “Obstacle” is not mentioned in the ITA.

Work Performed

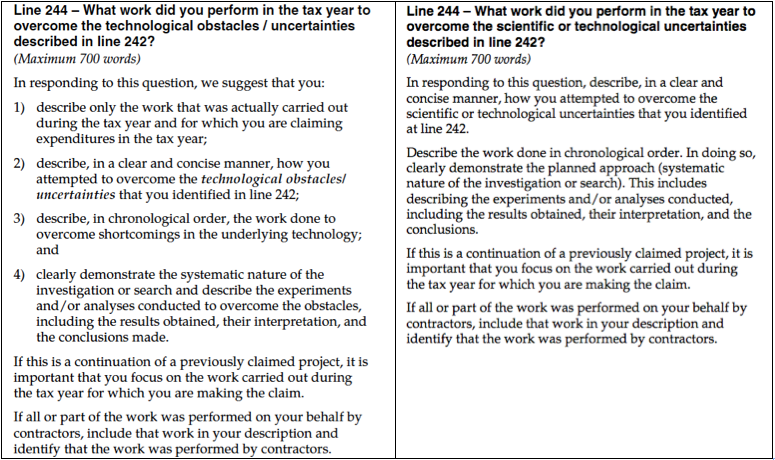

The new Line 244 instructions, while condensed, have not appreciably changed. The updated T4088 drops out the explicit mention of ensuring the work being described was performed in the tax year for which the claim is being filed, but this is still mentioned in Line 244 itself. The role for this section—to describe, in detail, the systematic SR&ED work for which the expenditures are being claimed—remains the same.

Comments are closed.