The SR&ED Tax Credit: A Program In Transition?

Reference Article (>5 Years Old)Please note that the information herein may be outdated, links could be inactive, and policies discussed may have evolved. For the most current data, consult our latest publications. If you would like us to refresh this article as it is of interest to you, please contact us. |

The winds of change are swirling around the Scientific Research & Experimental Development (SR&ED) program. In the past few months, there has been considerable debate around the way SR&ED is being overhauled and how strongly the effects will ripple through the industry. Below is a summary of the changes and the resulting impact—on everyone.

Changes to SR&ED

The changes have occurred in three waves: financial, policy, and administrative.

Financial

The 2012 budget saw several important changes to the program from a financial perspective. These included:

- Capital expenditures no longer eligible as of 2014.

- Prescribed Proxy Amount (PPA) reduced from 65% to 60% as of 2013, and again to 55% as of 2014.

- Claimable contractor costs reduced from 100% to 80% as of 2013.

- General ITC rate reduced to from 20% to 15% as of 2014.

Policy

In 2010, the CRA initiated a policy review project to “consolidate and clarify the SR&ED policy and related guidance documents that were current at that time.” The results from this were released December 2012, but the most significant residual effect was felt within the past two weeks: the release of the new T661 form.

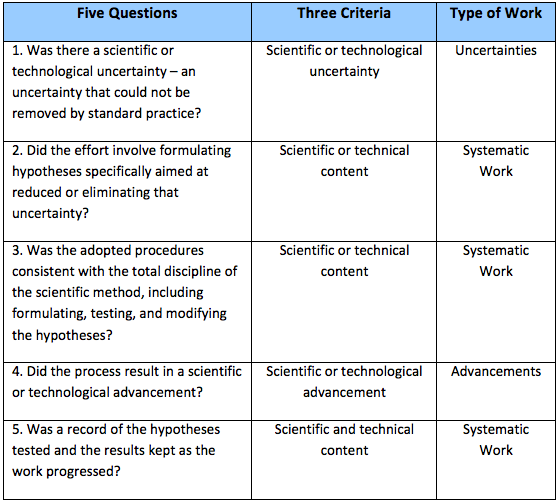

One outcome of the project was better alignment with legal precedents, most notably the inclusion of the “5 Questions” in policy documents. These hadn’t truly impacted the industry until the new form, as the wording of lines 242, 244, and 246—also known as the technical narrative—now reflects the “5 Questions” rather than the “3 Criteria” used beforehand.

Comparing the 5 questions to the 3 criteria.

Administrative

In the 2013 budget, additional initiatives were begun to improve the reliability of the program from an administrative perspective. These included:

- New pilot program introduced (e.g., Formal Pre-Approval Process).

- $5 million designated to CRA for “first-time claimant outreach.”

- $15 million designated to CRA for “reviews of SR&ED program claims where the risk of non-compliance is perceived to be high and eligibility for the SR&ED program unlikely.”

- The conclusion of the contingency fees report, which also influenced the new T661 form—failure to disclose who helped prepare your claim and what they charged will result in fines of $1000.

Consequences of SR&ED Changes

All companies claiming SR&ED will be affected—the question is to what degree.

Delays

With the additional $15 million for conducting reviews, many organizations are coming under scrutiny. While a technical or financial review will slow down the processing time for the organization involved, it also has a cascading effect on other groups. The sheer number of companies being examined is going to backlog an already lengthy process.

Reductions

The changes to eligible expenditures outlined in the 2012 budget will be strongly felt, either via the reductions to the Prescribed Proxy Amount (PPA), claimable contractor costs, or the general ITC. Additionally, more amounts may be disputed and disallowed during reviews due to the overarching policy and financial changes—an individual closely involved with program informed me that they have never seen claim size increase after a review.

How companies navigate these changes is going to guide where the SR&ED program goes from here. While it’s impossible to forecast what will happen, it is possible to be educated on the changes and adjust processes accordingly. Whether or not businesses, accountants, and consultants manage to effectively cope with the curveballs being thrown at them will determine if SR&ED will flourish or falter.