What is the Prescribed Proxy Amount (PPA) Cap?

Attention: Policies May Have Been Updated *** Some of the policies referenced were updated 2021-08-13. We are working to update this article and others. *** |

Cap?")

As many taxpayers typically opt to use the Proxy method to calculate their returns, we thought it pertinent to delve further into how to calculate the Prescribed Proxy Amount (PPA), what exactly the PPA Cap is, and how they may affect your claim.

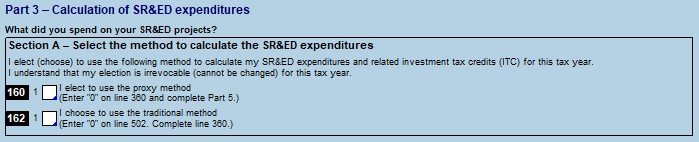

In the past, we have discussed the difference between the two choices available, Traditional and Proxy Method, to calculate your scientific research and experimental development (SR&ED) investment tax credits (ITCs). The traditional method is the default method selected when filing the Form T661, Scientific Research and Experimental Development (SR&ED) Expenditures Claim, you must check box 160 in Part 3 to select the proxy method. When the proxy method is selected, the Prescribed Proxy Amount (PPA) is calculated as a percentage of the salary base. According to the Prescribed Proxy Amount Policy, the PPA Cap is the overall cap or limit used to calculate the maximum PPA allowed to be claimed to ensure that the total eligible expenditures and deductions claimed (to include the PPA) are not greater than the total business expenditures made during the year.

Determining the Prescribed Proxy Amount

When using the proxy method you must determine your prescribed proxy amount. The SR&ED Glossary defines the PPA as:

The prescribed proxy amount is a notional amount on which SR&ED ITC can be earned. It is calculated as a percentage of a salary base. The PPA is only applicable when the claimant elects to use the proxy method.

The PPA is used in lieu of actual SR&ED overhead and other expenditures when calculating qualified SR&ED expenditures to earn SR&ED ITC. The PPA is not included in the pool of deductible SR&ED expenditures.1

As of 2014, the PPA is 55% of the salary base. The PPA is meant to represent overhead and business expenditures that may be deducted in a year as explained in the Traditional and Proxy Methods Policy.2 The PPA is often preferred as there is less paperwork required in keeping track of the overhead expenses for your SR&ED ITC. The PPA is calculated in Part 5 of the T661.

The Prescribed Proxy Amount Cap

To ensure the total qualified SR&ED expenditures and other deductions, including the PPA, are not greater than the total business expenditures made in the year the government of Canada established the Prescribed Proxy Amount Cap (PPA Cap). The PPA Cap is an overall cap or limit placed on a claimant’s PPA and is calculated based on the total expenditures for tax purposes minus certain deductions.

To determine your PPA cap, using your profit and loss worksheet is beneficial. The charts below illustrate how to determine your PPA cap.3

Income Statement

| Revenue | Calculation | Sub-total | Total |

|---|---|---|---|

| Sales | $100,000 |

||

| Expenses | |||

| Costs of goods sold | $10,000 | ||

| Purchases | ($5,000) | ||

| Ending inventory | |||

| Subtotal | $5,000 | ||

| Other expenses | |||

| Salary or wages (SR&ED expenditures) | $40,000 | ||

| Salary / Subcontractor Costs (non-SR&ED) | $6,000 | ||

| Interest | $2,000 | ||

| Utilities | $2,000 | ||

| Building rent | $5,000 | ||

| General administration | $2,000 | ||

| Depreciation | $10,000 | ||

| Subtotal | $67,000 | ||

| Total Expenses | $72,000 | ||

| Net income | $28,000 |

Net income (loss) for income tax purposes T2 – Schedule 1 (T2SCH1)

| Calculation | Total | |

|---|---|---|

| Net income per income statement | $28,000 | |

| Additions on Schedule T2SCH1 | ||

| Depreciation (line 104 of Schedule T2SCH1) | $10,000 | |

| Salary or wages (SR&ED expenditures) (line 118 of Schedule T2SCH1) | $40,000 | |

| Total additions | $50,000 | |

| Deductions on Schedule T2SCH1 | ||

| Capital cost allowance (CCA) from Schedule T2SCH8 | $5,000 | |

| SR&ED deduction claimed in year (line 411 of Schedule T2SCH1) | $20,000 | |

| Total deductions | ($25,000) | |

| Net income for income tax purposes | $53,000 |

Notes:

Salary or wages in the amount of $40,000 was reported as the total current SR&ED expenditures on line 380 of Form T661.

Overall cap on PPA

| Step 1: Total deductions for income tax purposes | |

|---|---|

| Total expenses per income statement | $72,000 |

| Less: Additions related to expenses per Schedule T2SCH1 | ($50,000) |

| Add: Deductions related to expenses per Schedule T2SCH1 | $25,000 |

| Total deductions for income tax purposes | $47,000 |

| Step 2: Deductions allowed under other sections of the Income Tax Act | |

| Interest | $2,000 |

| Capital cost allowance (CCA) from Schedule T2SCH8 | $5,000 |

| SR&ED deduction claimed in the year (line 411 of Schedule T2SCH1) | $20,000 |

| Total | $27,000 |

| Step 3: Deduction for the use of a building | |

| Building rent | $5,000 |

| Overall cap summary | |

| Step 1 – Total deductions for income tax purposes | $47,000 |

| Step 2 – Deductions allowed under other sections of the Income Tax Act | ($27,000) |

| Less: Step 3: Deduction for the use of a building | ($5,000) |

| Overall cap on PPA | $15,000 |

| Your PPA is the lesser of: | |

| a) the SR&ED PPA on line 820 of Form T661 ($40,000 × 55%) or | $22,000 |

| b) the overall cap on PPA as calculated above | $15,000 |

The amount left after subtracting the total of Step 2 from the total of Step 1, and then subtracting the total of Step 3 from the sum of the first equation (1-2=x) is the overall PPA Cap. It is important to ensure that your overhead costs exceed the proxy amount, otherwise, you will be subject to this PPA Cap. 4 In this example the tax software may automatically generate a PPA of $22,000 but the real PPA is $15,000 as it is subject to the PPA cap. If this is not correct, it is likely to trigger an audit at the CRA. Be sure to check that you are not subject to the PPA cap when you file.

Conclusion

The PPA Cap is meant to ensure the SR&ED expenditures made in the year are not higher than the total business expenditures made; however, if a claimant ensures their overhead costs match or exceed the PPA then they will not be subject to the PPA Cap and will be able to increase their end of year return. The Proxy method is often preferred as there is no need to track overhead and other expenditures for SR&ED. Both methods are beneficial, we recommend speaking with your SR&ED consultant and/or tax advisor to determine which method is right for your organization. To review our previous account of the two methods (Traditional and Proxy), how they differ from one another, and which one is right for you, please review our article “Proxy vs Traditional SR&ED Claim: Which Method to Choose”.

Connect With Us!

Share your thoughts by commenting below or joining the conversation on our LinkedIn page, Facebook page, or via Twitter.